Maritime satellite gets with the programme

Maritime communications spent a long time being of little interest to most people. Beyond safety requirements, it took the dotcom boom to generate a significant uptick in activity, as software entrepreneurs discovered this…

M2M and mad cows – through the mobility looking glass

Can satellite ever really go mainstream? It’s a nice idea, but one that has already claimed some scalps among those who have modelled the concept only to find the reality rather different.…

The VSAT challenge – be more like Inmarsat?

It’s DigitalShip Athens this week and a welcome chance to take the temperature of the comms market over two days of speeches, debate and I suspect, just a little alcohol. Looking at…

A carrot-shaped stick

Last week’s publication by investment bank Morgan Stanley of a report which polled three industry professionals on their views on FSS market prospects has caused a flutter or two, given its conclusion that…

Maritime HTS: revolution or business as usual?

To mark the publication of its most recent maritime analysis, Maritime Satellite Markets on Cusp of Bandwidth Revolution, I asked Senior NSR Analyst Brad Grady to give MaritimeInsight readers an introduction to…

‘Following a ship around with a satellite beam is not a business’

In part two of my conversation with consultant, analyst and blogger Tim Farrar, we dive a little deeper into the undergrowth: what the HTS upgrade path looks like and how to tell…

Not the end of history: some ruminations on maritime communications

Tim Farrar is an analyst and blogger who has been covering the satellite industry since the mid-1990s. We had crossed paths before, notably discussing his End of History blog and when he posted…

Owners speak – and you might not like everything they have to say

I was commissioned out of the blue earlier this year to write an article for Via Satellite magazine. I was flattered to be asked frankly – time for writing is a rare…

![]()

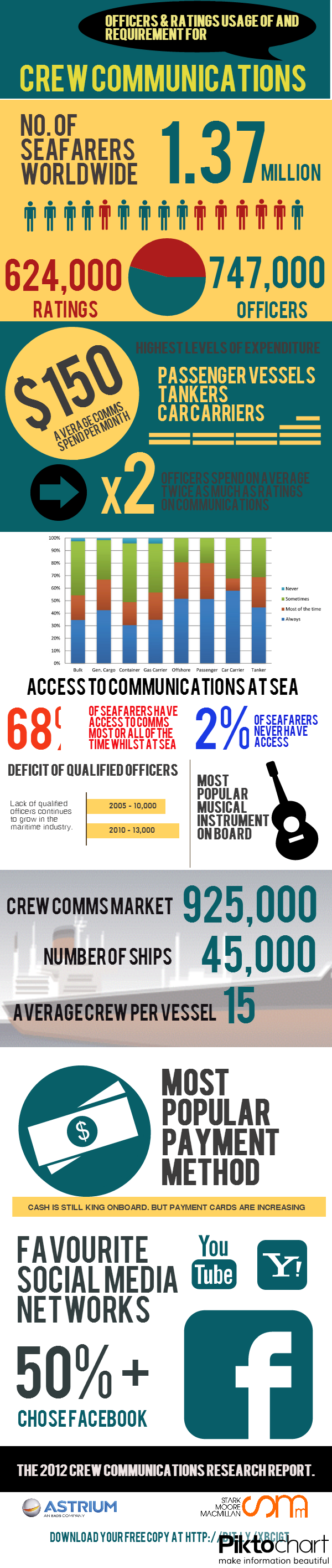

Crew retention is the tip of the digital iceberg

Almost 12 months ago an ambitious project began to take shape. Roger Adamson of Stark Moore Macmillan, Vizada (now Astrium Services) and two of the largest crewing agencies in the world, Philippine…

A year has gone by…

…since I started MaritimeInsight and March again finds me in Stamford once again, where the Connecticut Maritime Association moves and shakes for the next three days. Over the last year I’ve tried…

About

Neville Smith

Maritime Media Consultant to a roster of international shipping industry clients. Former maritime journalist with 16 years’ experience reporting the shipping and marine insurance markets and former Deputy Editor at Lloyd’s List, I assist clients with matching their communication needs to publications and media channels that gain them their desired level of exposure.

From our Twitter

Sagitta Marine Managing Director Thomas Zaidman thinks the #Handysize and #Supramax segments could see positive fortunes for the balance of 2024 thanks to firm demand and lingering market risks, reports @drycargomag

https://www.drycargomag.com/sagitta-marine-forecasts-volatility-and-opportunity-for-small-bulker-sector

#drybulk #commodities #panamacanal

Again.

Must admit I felt a little low this morning. So I did what I always do in these circumstances and sought out the Dr Hedgeh note. There now! Feeling much better.

Always works.

Baku Shipyard has agreed a new deal to implement the ShipConstructor design and modelling software system from @SSI_CAD, to support new digital workflows and improve efficiency and precision in its #shipbuilding projects.

The key to understanding the dark fleet/sanctions conundrum is that compliant players in the shipping industry are over-regulated and the non-compliant ones aren't regulated at all.