![]()

Crew retention is the tip of the digital iceberg

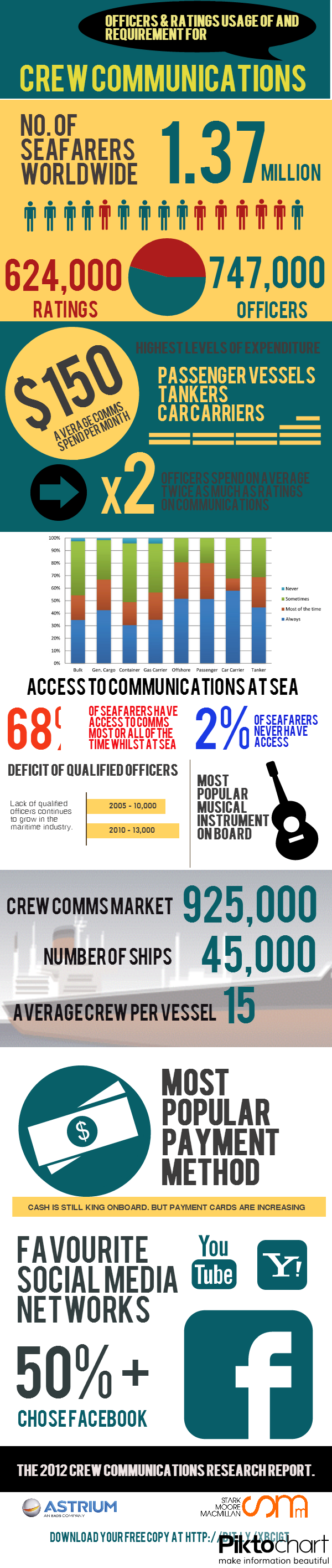

Almost 12 months ago an ambitious project began to take shape. Roger Adamson of Stark Moore Macmillan, Vizada (now Astrium Services) and two of the largest crewing agencies in the world, Philippine…

Epic stuff – James Collett on Intelsat, Inmarsat and what really matters in maritime

To leafy Chiswick in West London and the offices of Intelsat for a wide-ranging conversation with James Collett, late of Inmarsat and now Director of Mobility Services at Intelsat, charged with building…

About

Neville Smith

Maritime Media Consultant to a roster of international shipping industry clients. Former maritime journalist with 16 years’ experience reporting the shipping and marine insurance markets and former Deputy Editor at Lloyd’s List, I assist clients with matching their communication needs to publications and media channels that gain them their desired level of exposure.

From our Twitter

Sagitta Marine Managing Director Thomas Zaidman thinks the #Handysize and #Supramax segments could see positive fortunes for the balance of 2024 thanks to firm demand and lingering market risks, reports @drycargomag

https://www.drycargomag.com/sagitta-marine-forecasts-volatility-and-opportunity-for-small-bulker-sector

#drybulk #commodities #panamacanal

Again.

Must admit I felt a little low this morning. So I did what I always do in these circumstances and sought out the Dr Hedgeh note. There now! Feeling much better.

Always works.

Baku Shipyard has agreed a new deal to implement the ShipConstructor design and modelling software system from @SSI_CAD, to support new digital workflows and improve efficiency and precision in its #shipbuilding projects.

The key to understanding the dark fleet/sanctions conundrum is that compliant players in the shipping industry are over-regulated and the non-compliant ones aren't regulated at all.