How hard will OPEC’s production cuts hit tanker markets in 2017?

![]() After a year of political and policy upheaval, both oil and tanker markets are undergoing a process of rebalancing, writes Tim Smith, Senior Analyst, Maritime Strategies International

After a year of political and policy upheaval, both oil and tanker markets are undergoing a process of rebalancing, writes Tim Smith, Senior Analyst, Maritime Strategies International

The fourth quarter of 2016 capped what has been a mixed 12 months for the tanker markets. The agreement by OPEC members and non-OPEC alike to reduce production in an attempt to reduce oversupply will be a core determinant of conditions in 2017. The latest MSI Quarterly Tanker Market analysis* finds that despite the cuts having a negative near-term impact, there are reasons to be positive on prospects for the longer-term.

Despite some seasonal upside in the final period of the year, 2016 has undoubtedly been a year of negative dynamics across the tanker industry. This has been the case both in terms of the annual change in freight rates, which has been universally negative against 2015, and asset prices, on which the twin gravitational forces of lower newbuild prices and lower earnings have acted forcefully.

Compared to other shipping sectors, the last couple of years in the tanker market have seen a distinct lack of trend. Markets have move up rapidly and then retreated at almost the same speed. Volatility and uncertainty over the shifting landscape of the oil market have been reflected and amplified in the tanker freight market.

Oil markets are now returning to more ‘normal’ conditions, with OPEC having put in place restrictive output policies, which should act to support crude prices and accelerate stock draws already evident in Q4.

Oversupply of productive capacity in the oil market has been mirrored by excess tonnage capacity in the tanker market. Both are now rebalancing and although fleet growth is expected to remain high in 2017, low earnings and the ratification of ballast water treatment regulations support MSI’s expectations that tanker scrapping will move sharply higher in 2017.

This will help construct a market recovery in 2018 and beyond, built on much lower fleet growth rates than being seen currently, both in the large crude and product tanker sectors.

Relative restraint in Middle East crude production during 2017 has been and remains an implicit element of the MSI Base Case. OPEC’s decision to cut output remains fraught with uncertainty on how the group will manage to maintain discipline and encourage non-OPEC participants to join in. Moreover, the cut is not especially big.

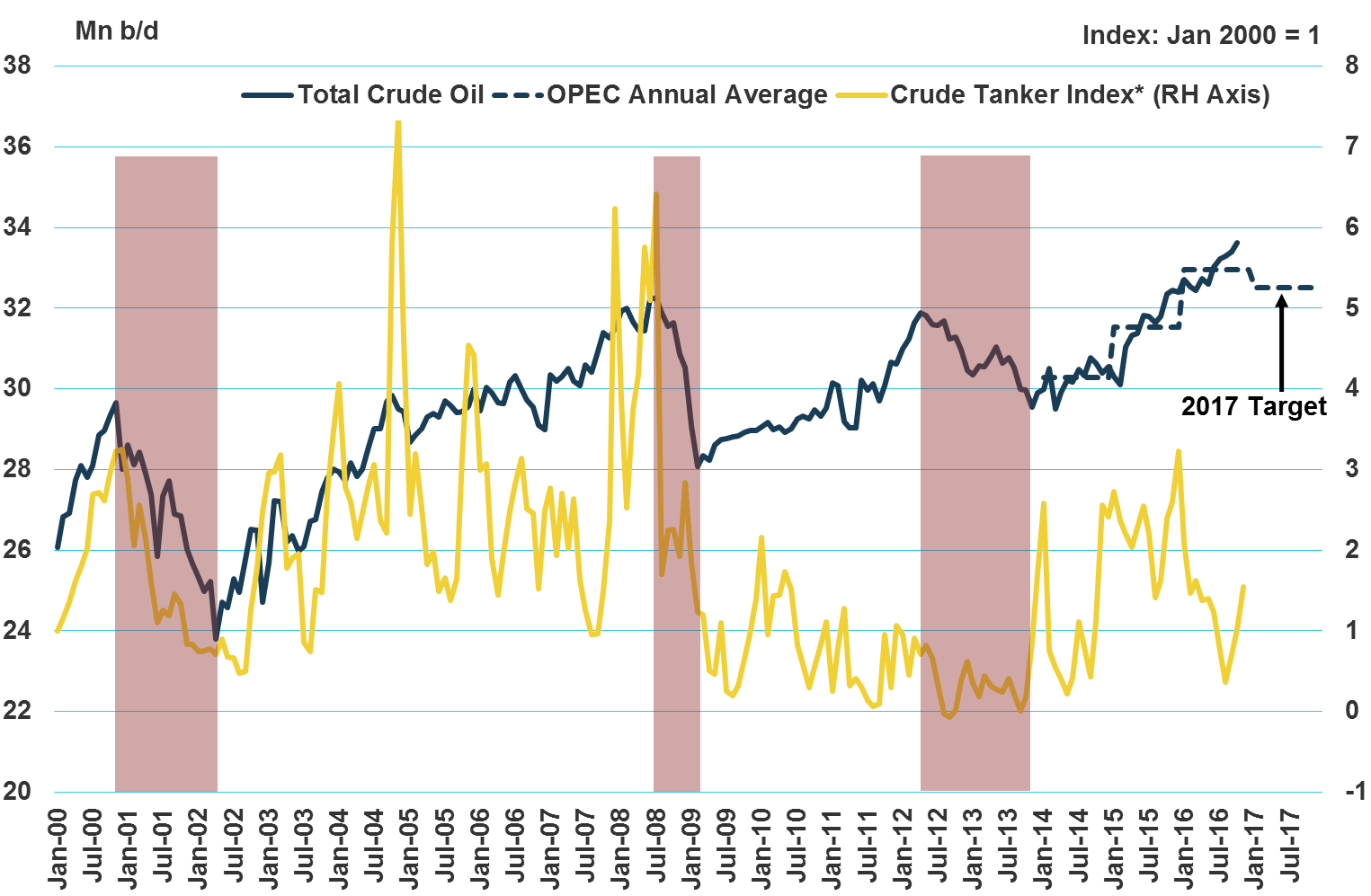

Chart 1 below shows that periods of actual decline in OPEC crude production in the last 15 years have always been accompanied by a decline in crude tanker freight rates.

Looking at the last three major reductions in OPEC production which began in 2000, 2008 and 2012 from peak to trough, the outcome is more important than the intent, as will be the case for the latest efforts to support prices.

In these three instances the relative declines over the highlighted periods were 20%, 13% and 7% from monthly average peak to trough. The agreement OPEC has reached is to cut output by 1.2 Mn b/d from October levels which according to IEA data was 33.6 Mn b/d.

*Includes VLCC, Suezmax, Aframax spot benchmarks

Chart 1: OPEC Crude Production and the Crude Tanker Market.

This provides a framework to look at OPEC’s production cut in context. Included in Chart 1 are the annual average OPEC production levels over the last three years (2016 is January- October) with the implied target level of 32.5 Mn b/d. The drop between 2016’s annual average and 2017’s, assuming this is maintained across the year – and the initial proposal is for the first six months – is just 1.4%.

Should this succeed the profile will be more dynamic – taking a similar peak-to trough approach MSI estimates a drop of 3%, perhaps stretching to 5%. This will be joined by non-OPEC producers, led by Russia, aiming to reduce combined production by 600,000 b/d.

It is difficult to put a positive slant on these actions, reinforcing our expectations for weaker tanker earnings levels in 2017 versus 2016. Even so, MSI cautions on becoming too bearish, given the relatively light cut by OPEC, prospects for crude coming out of the US and potential improvement in the refining sector, should the oil glut be alleviated.

/…more

This latter process has been protracted and downside risks of high fleet growth, a relapse in Chinese demand and broader macroeconomic malaise resulting from e.g. intensified protectionist measures are still present, and could still push 2017 substantially lower than the MSI Base Case.

The tanker market, like the oil market, is in a clearing phase, removing over-supply and rebalancing. That process could take another year or so before returning to a position where sustained gains can be made, but we remain positive on the long-term outlook.

The MSI analysis concludes that one-year time charter rates are close to a floor in terms of Q4 levels, with much of the downward dynamic having already occurred in 2016. 2017 will be low but will see more restrained downward movements.

Over the course of this year MSI has steadily downgraded forecast newbuilding prices, while keeping the same general evolution of the forward curve. In Q4 revisions to the near-term have been relatively limited, as we approach a price floor below which we believe few shipyards are willing/able to venture with forward cover (estimated time to complete current orderbook) at Asian yards of 1.6 years.

On the cost side of the shipbuilding equation, other trends have generally acted to undermine newbuilding prices, with steel plate driven lower this year by massive oversupply in capacity which has disconnected price evolution from the trend in broader semi-finished steel products.

The currency markets, while always volatile, have been in turmoil, with events conspiring to send most key currencies in the opposite direction to expectations. In Asia the trends have been significant with implications for shipbuilders across the region. Asian currency turmoil reflects to some extent the impact on Asian emerging markets of Trump’s US election victory.

As a result, second-hand prices will struggle with the combined weight of both falling newbuilding prices and the continued deterioration in vessel earnings during 2017.

Ends

About Maritime Strategies International

Since its inception in 1986, Maritime Strategies International (MSI) has established itself as one of the shipping industry’s foremost independent research and consultancy firms. Our success is built on a strong focus on maritime economics and econometric modelling. We provide a comprehensive range of advisory services, including forward valuations market forecasts, reports and commercial consultancy services for all shipping sectors. MSI asset price forecasts are used by ship finance providers holding 40% of all shipping bank debt and we provide analytical and methodological support to give the context and credence to our results. For more information please see www.msiltd.com

* The MSI TSPS Tanker Report was produced using MSI’s proprietary forecasting models and expert technical analysis. The quarterly report is available on request and MSI experts are available for interview. For further information please contact Neville Smith, Mariner Communications Tel: +44 7909 960 182.